Findings show that the United States owes more than $36 trillion while Nigeria owes over N159.28 trillion, with external debt now standing at approximately $51.8 billion. At a first glance, when comparing the debt profiles of the world’s largest economy and Africa’s largest economy, it may though seem misplaced. America can borrow almost indefinitely because it issues the world’s reserve currency. Nigeria cannot. Yet both countries are confronting a similar worry.

This has led to asking: When does debt cease to be a tool for development and become a permanent feature of national survival?

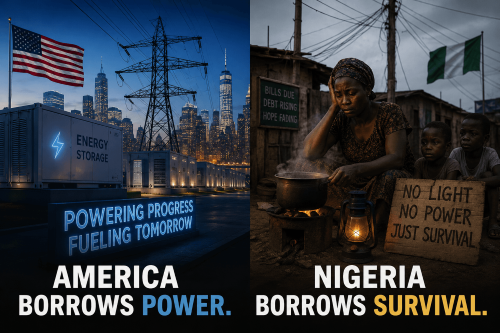

The difference is that while America may be testing the limits of how much debt a superpower can carry, Nigeria is testing how much debt a fragile developing economy can sustain before it begins to mortgage its future.

The latest proposal by the Federal Government to secure another $1.25 billion World Bank facility under the Nigeria Actions for Investment and Jobs Acceleration Programme has once again reignited a debate that refuses to disappear. What appears to be far from the daily lived experience of Nigerians over the years, is having government officials insisting that the loan will support investment, expand access to finance, improve electricity, enhance digital services, and create jobs. According to the claims, these are worthy objectives. But Nigerians have heard similar promises before.

The more important question is no longer whether Nigeria should borrow. Virtually every modern economy borrows. The real question which calls for critical concern, is what exactly Nigeria is borrowing for, and why the benefits of decades of borrowing remain largely invisible in the everyday lives of millions of citizens. This is where the national conversation becomes uncomfortable.

Funny enough over the years, successive governments have justified borrowing as a necessary response to development deficits. Yet despite rising debt levels, many Nigerians struggle to identify corresponding improvements in their lived experiences. This justification has kept many wondering as the roads remain dilapidated, public hospitals are overwhelmed, electricity supply also remains unreliable. Talk of the public education system, this has continued to deteriorate badly and unemployment remains stubbornly high. Inflation has eroded incomes with the cost of cooking gas hitting N2,400 per kg, while businesses struggle under the weight of high operating costs.

If borrowing is supposed to finance development, where is the development? The concern becomes even more urgent and highly alarming when viewed against the backdrop of Nigeria’s worsening fiscal position. According to the Debt Management Office, public debt has climbed to over N159 trillion. With this outrageous figure, more troubling is the fact that debt servicing now consumes an alarming share of government revenue, which has continued to cripple economic growth and compromise the future. This development caught the attention of the Nigerian Economic Summit Group as it recently noted that Nigeria’s debt-service-to-revenue ratio remains among the highest in the world. In simple and practical terms, this implies that the government is spending an increasingly large portion of what it earns paying creditors rather than investing in infrastructure, healthcare, education, security, or economic expansion.

This is the hallmark of a debt trap. The danger is not necessarily that Nigeria will default tomorrow. The danger is that the nation becomes trapped in a vicious cycle where governments borrow to finance deficits, then borrow again to service existing obligations, and then borrow even more to cover the consequences of previous borrowing. That cycle is already becoming visible.

Come to think of it, President Bola Tinubu’s administration has boldly defended borrowing as necessary to support reforms, cushion economic shocks, and stimulate growth. Yet critics have continued to point to the fact that since May 2023, borrowing has accelerated significantly.

According to economic analyst, Dele Oye, the current administration has added approximately N65.9 trillion to Nigeria’s debt stock within just two years, a figure that exceeds several multiples of what Nigeria accumulated during its first five decades after independence.

Whether one agrees with the politics surrounding that claim is secondary. The underlying concern remains valid since debt is growing far faster than the visible capacity of the economy to generate sustainable revenue. This is why comparisons with the United States are useful.

America’s debt is enormous, but debt sustainability is not determined by the size of debt alone. It is determined by economic productivity. The United States supports its debt burden through a diversified economy, deep capital markets, technological innovation, globally competitive corporations, advanced research institutions, and an unmatched ability to attract global investment.

Debt is not what sustains America. Productivity does. Unlike Nigeria and by contrast, it continues to rely heavily on crude oil revenues, a narrow tax base, volatile foreign exchange earnings, and a fragile manufacturing sector. The critical difference is that every dollar borrowed by Nigeria therefore carries greater risks than every dollar borrowed by the United States.

When America borrows, it borrows largely in its own currency. When Nigeria borrows externally, it exposes itself to exchange-rate risks that can dramatically increase repayment costs whenever the naira weakens as this calls for utmost caution. Every currency depreciation effectively inflates the burden of external obligations. What appears manageable today can become overwhelming tomorrow. This reality makes Nigeria’s current debt trajectory particularly concerning which is but the truth.

The World Bank itself has raised concerns about governance risks and structural weaknesses within Nigeria’s fiscal architecture. Even more troubling are recent revelations indicating that more than N34.5 trillion was reportedly deducted through pre-distribution mechanisms before revenues reached the Federation Account between 2023 and 2025. According to the findings, approximately 41 percent of government revenues were removed as first-line charges before distribution.

Whichever way it is viewed, perhaps as fiscal leakages, weak oversight, or institutional inefficiency, the implications are profound and of critical concern. If we must begin to tell ourselves the factual truth, a nation cannot continue borrowing aggressively while simultaneously failing to maximise the value of revenues it already generates.

This brings us to the central question confronting Nigeria today. The point is, are these loans building future productive capacity, or are they merely financing continuity?

Borrowing can be justified when it funds projects that expand economic output. Investments in power generation, transport infrastructure, agriculture, industrialisation, technology, and education can create long-term growth that eventually pays for the debt itself. In such cases, debt becomes a bridge to prosperity.

But it must be known that borrowing to fund recurrent expenditure, sustain bloated government structures, finance consumption, cover inefficiencies, or service previous debts transforms borrowing into a treadmill. The irony here is that the country runs harder every year but remains trapped in the same place. Unfortunately, much of Nigeria’s fiscal reality increasingly resembles the latter.

The tragedy is that this debt burden is not abstract. It is already affecting ordinary Nigerians. The adverse implication and critical point are that every naira directed toward debt servicing is a naira unavailable for schools, hospitals, security, electricity, or social protection. Every external loan increases future repayment obligations. Every missed opportunity to invest borrowed funds productively transfers today’s policy failures to future generations.

{kind=link}